Imagine you go to the emergency room for chest pain. After treatment, you’re handed a stack of papers to sign-your consent for treatment, your agreement to pay, and a pre-filled application for a medical financing plan like CareCredit®. You’re in pain, tired, and just want to go home. You sign everything. Months later, you find out you’ve been charged $8,000 for a procedure you thought was covered, and your credit score has dropped because the hospital reported the bill to a collection agency. This isn’t rare. It’s the reality for millions of patients-until recently.

Why Patient Protection Laws Are Changing

In 2024, New York State passed three groundbreaking laws aimed at stopping predatory financial practices in healthcare. These weren’t minor tweaks. They rewrote how doctors, hospitals, and clinics interact with patients when it comes to money. The goal? To stop patients from being tricked into debt they didn’t understand-and to make sure they know exactly what they’re agreeing to before any treatment begins. The data behind this shift is alarming. According to the Consumer Financial Protection Bureau, over 100 million Americans carried $195 billion in medical debt in 2023. Nearly 1 in 10 people under 65 had medical bills in collections by 2022. These aren’t just numbers-they’re people skipping meals, delaying care, or losing homes because of hospital bills. These laws didn’t come out of nowhere. They followed the federal No Surprises Act, which took effect in January 2022 and banned surprise bills from out-of-network providers. But that law didn’t fix everything. It didn’t stop hospitals from pushing patients into high-interest financing plans. It didn’t stop them from asking for credit card details before emergency care. And it didn’t stop them from combining consent for treatment and payment into one form, leaving patients unaware they were signing up for debt.Three New Rules That Protect You as a Patient

Starting October 20, 2024, New York hospitals and clinics had to follow three new rules. These are now the strongest patient financial protections in the country-and they’re setting a national example.- Separate Consent for Treatment and Payment

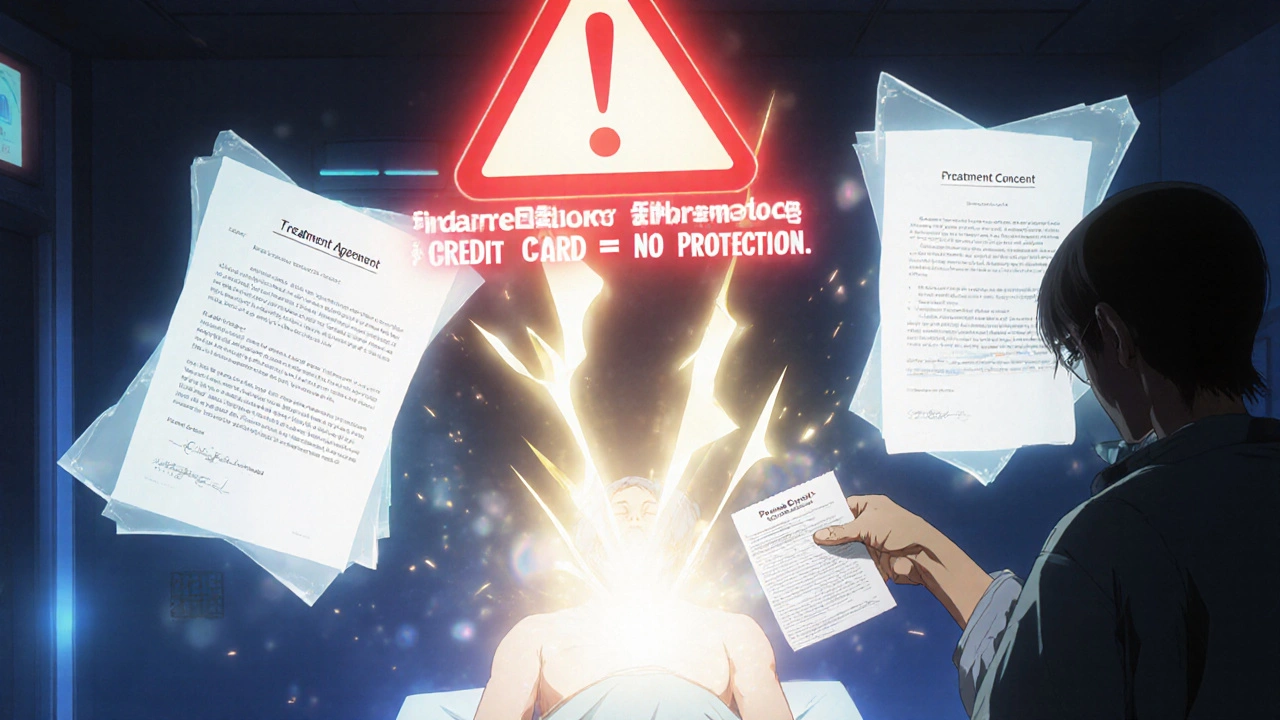

Before, providers could make you sign one form that covered both your treatment and your agreement to pay. Now, they must give you two separate documents. One says you agree to receive care. The other says you agree to pay for it. You have to read, understand, and sign each one on its own. If they don’t, they can be fined $2,000 per violation. - No More Pre-Filled Financing Applications

Hospitals can no longer hand you a CareCredit® application and help you fill it out-even if they say they’re just "helping." The law says the patient must complete the entire form themselves. Staff can answer questions like, "What’s the interest rate?" or "How long is the term?" But they can’t touch the pen, click the buttons, or suggest you sign up. Violations can cost up to $5,000 per incident. - No Credit Card Preauthorization for Emergencies

Hospitals can no longer demand your credit card number before giving you emergency care. They can’t keep your card on file. And if you do pay with a regular credit card, they must give you a written warning: "Using a credit card for medical bills means you lose protections against wage garnishment, liens, and credit reporting."

These rules exist because there’s a dangerous gap in protection. If you use a medical financing plan like CareCredit®, you get legal safeguards: no credit reporting, no wage garnishment, no liens on your home. But if you use a regular Visa or Mastercard? You get none of that. You’re treated like any other consumer debt-meaning collectors can come after your paycheck, your bank account, even your house. New York’s law forces providers to make that difference crystal clear.

What This Means for You

You don’t need to be a lawyer to use these laws. Here’s what to do when you’re in a healthcare setting:- Always ask for separate consent forms. If they hand you one paper with both treatment and payment, say, "I need to review these separately."

- Never let anyone fill out a financing application for you. If a staff member offers to help, say, "I’ll complete it myself." If they insist, report it to the New York State Department of Health.

- Refuse to give your credit card before emergency care. No matter how urgent it is, they can’t legally require it. If they do, write down names, times, and what was said. You have rights.

- Ask for the warning about credit cards. By law, they must give it to you in writing if you pay with a regular card. If they don’t, ask again. If they still refuse, file a complaint.

These protections apply whether you’re insured or not. Even if you have Medicare or Medicaid, these rules still cover how you’re asked to pay for services.

What’s Still Unclear

There’s one big problem: confusion. In August 2025, a legal advisory from Goldsand Friedberg said the rule requiring separate consent (Public Health Law Section 18-c) had been suspended. That means some hospitals may still be using the old, combined forms-and they might think they’re allowed to. The New York State Department of Health hasn’t officially confirmed the suspension. So right now, you’re in a gray zone. If you’re unsure whether a provider is following the law, call the Department of Health’s Patient Protection Hotline at 1-800-442-2203. They can tell you if the rule is active in your area.

What This Means for the Future

New York isn’t alone in this fight. The CFPB removed medical debt from credit reports in 2024. That was a huge win. But it didn’t stop providers from pushing patients into debt traps. New York’s laws go further. They attack the system at its root: the way money is handled during care. Experts believe other states will copy these rules. California, Illinois, and Massachusetts are already reviewing similar bills. If you live outside New York, don’t assume these protections don’t apply to you. They might soon. The trend is clear: healthcare is no longer just about medicine. It’s about financial fairness. And patients are finally getting a voice.What You Can Do Now

If you’ve been hit with a surprise medical bill or forced into a financing plan you didn’t understand, you’re not alone-and you’re not powerless.- Request a detailed itemized bill from your provider. By law, they must give it to you within 30 days.

- Check if the bill was reported to a credit agency. If so, dispute it. Under the CFPB’s 2024 rule, medical debt must be removed from credit reports if it’s paid or settled.

- If you signed a combined consent form in New York after October 20, 2024, you may have grounds to challenge the payment terms. Contact a legal aid organization like Legal Services NYC for free help.

- Spread the word. Tell friends, family, and support groups about these rights. Most patients still don’t know they exist.

Healthcare shouldn’t bankrupt you. These laws are a start. But they only work if you know them-and use them.

Do these New York patient protection laws apply to me if I live outside New York?

These specific laws only apply to healthcare providers operating in New York State. However, the federal No Surprises Act and the CFPB’s medical debt removal rule apply nationwide. Many other states are now considering similar laws based on New York’s model. If you’re receiving care in New York-even if you’re from another state-you’re protected under these rules.

Can a hospital refuse to treat me if I don’t sign a financing agreement?

No. Under New York law and federal emergency care rules, providers cannot deny treatment because you refuse to sign up for CareCredit® or another medical financing plan. This applies to both emergency and non-emergency care. If they threaten to delay or refuse care, document the interaction and report it to the New York State Department of Health.

What’s the difference between CareCredit® and a regular credit card for medical bills?

CareCredit® and similar medical financing plans are designed specifically for healthcare. They often offer interest-free periods and are protected under New York law from wage garnishment, liens, and credit reporting. Regular credit cards-like Visa or Mastercard-offer none of these protections. If you pay a $10,000 hospital bill with a credit card, the provider can report it to collections, garnish your wages, or even place a lien on your home. With CareCredit®, they can’t.

What should I do if a hospital staff member fills out a financing form for me?

Stop the process immediately. Tell them you’re aware of the law and that they’re violating it by completing the form. Ask for a supervisor. If they continue, write down their name, time, and what happened. File a complaint with the New York State Department of Health at health.ny.gov or call 1-800-442-2203. You can also report the incident to the Consumer Financial Protection Bureau.

Are there any exceptions to the credit card rules?

Yes. Providers can ask for credit card information for scheduled, non-emergency procedures-like elective surgery-if they give you the required written warning about risks. But even then, they can’t require it as a condition of service. For emergency care, no credit card information can be collected before treatment. This includes urgent care centers, ambulances, and hospital ERs.

Elaina Cronin

21 November, 2025 . 21:41 PM

This is a systemic betrayal of human dignity. Hospitals are predatory lenders disguised as healers. The fact that patients are forced to sign combined consent forms while in pain is not negligence-it’s malice. I’ve seen it happen to my sister. She signed under duress, and now she’s being hounded by collectors. This law is not generous-it’s corrective. And if any hospital in New York is still using old forms, they should be shut down. Immediately.

Willie Doherty

23 November, 2025 . 10:40 AM

Let’s analyze the statistical impact: prior to the 2024 legislation, medical debt collection rates in New York were 14.3% higher than the national average. The separation of consent forms reduces-but does not eliminate-risk. The real issue is enforcement. Only 12% of patients report violations. And the fines-$2,000 to $5,000-are negligible compared to the average $8,000 bill. This is performative regulation. The CFPB’s removal of medical debt from credit reports was substantive. This? A PR maneuver.

Darragh McNulty

25 November, 2025 . 08:52 AM

YESSSS!! 🙌 This is what change looks like!! I’ve been screaming about this for years-patients shouldn’t have to be finance experts just to get treated! 🏥💙 If you’re reading this and you’ve ever been pushed into CareCredit® while crying from pain-you’re not crazy. You were manipulated. And now? You’ve got power. Share this. Text your mom. Post it on Facebook. Let’s make sure NO ONE gets screwed like this again. 💪❤️

David Cusack

26 November, 2025 . 00:06 AM

One must consider the ontological implications of consent in a capitalist medical-industrial complex… The separation of treatment and payment documents is merely a syntactic gesture-devoid of semantic substance-unless the underlying economic structure is dismantled… The state, in its infinite wisdom, regulates the symptom… while ignoring the disease… Capital… is the true provider…

Julia Strothers

26 November, 2025 . 17:30 PM

So now New York is playing socialist doctor? Who funded this? Soros? The WHO? This is the first step to government-run healthcare-forcing hospitals to hand out forms like they’re handing out free condoms. Next they’ll ban credit cards entirely. And don’t even get me started on how this opens the door for illegal immigrants to get free ER care while Americans go bankrupt. This isn’t protection-it’s exploitation by another name.

Erika Sta. Maria

27 November, 2025 . 20:52 PM

Wait… so you’re saying if I go to a hospital in Mumbai and they ask for my credit card I’m protected? No? Then why are we even talking about New York? This is cultural imperialism disguised as policy. In India we just pay cash or barter. One time I paid a doctor with two goats. He fixed my knee. No forms. No debt. No drama. Also, CareCredit? Sounds like a scam name. Like AppleCare but for bills. LOL

Nikhil Purohit

29 November, 2025 . 12:41 PM

Man, I’m so glad this is getting attention. I work at a clinic in Delhi and we’ve got patients coming back with debt from U.S. hospitals they visited on vacation. They don’t even know they signed up for financing. This law? It’s a blueprint. Simple, clear, human. I’m sharing this with my whole family. My aunt just had surgery last month-she didn’t know she could say no to handing over her card. Now she will. Thanks for writing this.

Chris Vere

29 November, 2025 . 19:10 PM

It’s interesting how the law focuses on form rather than intent. The real problem is not that forms are combined-it’s that patients are not given time to think. The system is designed to rush. Even with separate documents, if you’re in pain, you’re still vulnerable. The law helps, but it doesn’t heal. What we need is compassion. Not more paperwork. Just… kindness.

Pravin Manani

30 November, 2025 . 04:01 AM

From a healthcare economics standpoint, the structural asymmetry between medical financing instruments and consumer credit is a critical gap in consumer protection architecture. The absence of regulatory parity between CareCredit® and Visa/Mastercard creates a regulatory arbitrage opportunity for providers-essentially enabling debt migration from protected to unprotected instruments. The New York statute closes this loophole via informational asymmetry reduction, thereby restoring pareto efficiency in patient-provider financial transactions. This is a landmark in behavioral health finance policy.